The Hormuz Shock Déjà Vu: Why This One Could Be Bigger than 2022

A quick reaction and a few high-level observations on the global energy shock unfolding from Iran, specifically on natural gas and LNG markets impacts - why this could be worse than 2022.

Tatiana Khanberg

3/3/20262 min read

The Hormuz Shock Déjà Vu: Why This One Could Be Bigger than 2022

A quick reaction and a few high-level observations on the global energy shock unfolding from Iran, specifically on natural gas and LNG. Using general rounded numbers for scale.

The 2022 Russia-Ukraine supply shock gave the energy market time, albeit still short, to adjust. What's happening now at the Strait of Hormuz has been overnight.

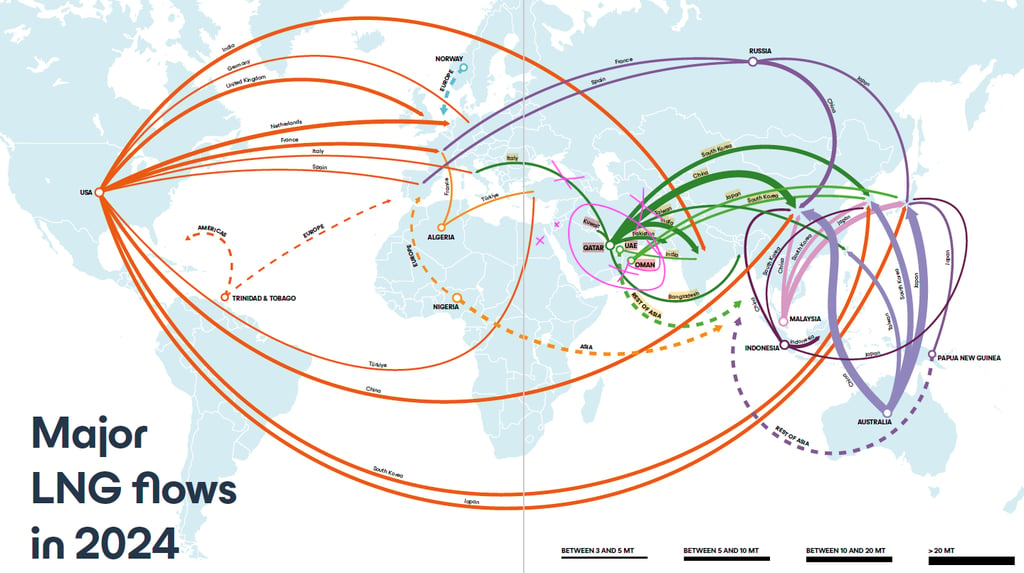

Together, Qatar, UAE, and Oman exported approximately 130 bcm of LNG in 2024. For scale: the volume of gas lost from Russia after February 2022 was roughly 100–120 bcm. The critical difference is that the Russian supply disruption played out over months. This one happened overnight.

Green flows indicate directly impacted outflows. Source: 2025 GIIGNL Annual Report.

This looks likely to produce a bigger ripple than the 2022 shock, particularly if the conflict continues for a longer period, which is looking increasingly probable.

There's been some speculation about which markets will bear most of the brunt. However, at this scale, the answer is - all of them. It is true that the markets directly receiving Qatari gas (mostly in Asia), or other shipments routed through Hormuz, are the first point of impact, and it will hurt. That said, with Qatar being the second-largest LNG exporter in the world, after the United States, a shutdown of QatarEnergy's production removes a volume on the order of ~106 bcm (based on 2024 data) from the market, which is comparable to what Russia's war gradually stripped out over its opening months, except this is compressed into just over 72 hours days.

No market is truly insulated from that kind of volatility, because there is no immediate replacement. As in 2022, the knock-on effects will extend to gas-dependent feedstock industries, including fertilizers. Prices will rise.

Beyond Qatar, there are additional, smaller but still material supply points affected: UAE, Oman, and Israel, which supplies both Egypt and Jordan.

Europe enters this with gas storage at roughly 30% -- just above where it stood in March 2022 -- meaning European buyers will be competing aggressively to fill reserves ahead of next winter, but some, like Germany are even lower on storage and will need more gas more urgently.

What about Russia?

Russia stands to benefit from higher prices, and it holds replacement gas volumes that could theoretically cover the gap. In practice though, that gas cannot go anywhere fast. Sanctions constrain both gas and oil exports; the Nordstream pipelines are destroyed; LNG infrastructure projects to boost capacity remain delayed, and the EU has now passed its first-ever law specifically prohibiting Russian gas imports (pipeline gas as of March 2026, all forms by January 2027.)

On a personal note: this situation brought up a bit of gloomy déjà vu, with its timing just four days after the four-year anniversary of the start Russia's operation in Ukraine

One broader observation worth sitting with: the world has developed a strange new concept of the "timed war." In recent days, much of the attention has been on waiting for Washington to confirm the exact duration of the engagement. History offers little confirmation for the idea that wars submit easily to scheduling. I'll leave that thought there for now.

Subscribe to the situation room newsletter

Building Smarter Energy Communications

© 2026. All rights reserved.

Send us a message, or

Ready to lead your own narrative? Book a free discovery call, or send us an email.

contact@statem.net