The Electrification Wager | Strategic Energy Briefing | July 13

Your weekly strategic energy briefing: the stories that shape global energy narrative in which you operate. Situational intelligence for oil, gas, and energy executives who want to lead their own narrative.

CONTEXTNEWS & NARRATIVEANALYSIS

7/13/20269 min read

The Electrification Wager

Subscribe and get the briefing in your inbox each week.

TL;DR

The European Commission publishes its Electrification Action Plan on Friday, July 17th; a leaked draft has been covered extensively. The plan casts converting fossil fuel demand to electricity as a security, competitiveness and industrial imperative, with a 32% by 2030 electrification commitment already on the books and a binding target expected later this year. Industry is split: an alliance of electrification players wants binding targets, while energy-intensive industries want the plan judged on delivering €50/MWh industrial electricity instead. The blind spots to watch: demand creation does not guarantee domestic industry, and Europe's clean-tech base is thin (about 2% of manufacturing value added) while the existing industrial base erodes; the technology mandates contradict the plan's own neutrality language; moving the "tax portion" off electricity bills shuffles costs without addressing their cause; and the €200 billion import-savings case comes without a visible cost-benefit assessment. Meeting the target implies more than 460 GW of new firm capacity, while at least 120 GW of renewables already cannot connect due to grid constraints. The main thing to watch on Friday: how much becomes binding instruments versus aspiration.

Context

This week was full of major developments, and I am testing a new deeper-dive format to add a focus – tell me what you think, and if you find it useful, the best compliment is forwarding it to someone who might too.

Just as things seemed to be looking up in the Gulf, the ceasefire collapsed and Hormuz is closed again, while in Russia, Ukrainian attacks on fuel infrastructure intensified. Both add decibels to the alarm in the energy and commodities supply crisis, while the "temporary disruption" narrative is getting shaky in the fifth month of the confrontation in the Gulf. China has now banned helium export, and Russia banned diesel export. And as the push to substitute fossil fuels with electricity grows stronger in response, the IGU's LNG report showed record trade up 6.3% to 437 million tonnes in 2025, with much of it absorbed by Europe replacing lost Russian pipeline volumes. Last year also had the highest LNG supply investment since 2019, so large new quantities of LNG are undoubtedly on their way, but where they go and at what price is less certain, not least due to the focus of today’s newsletter.

Ahead of this week’s release of the Electrification Action Plan (EAP), expected on July 17th, the narrative of converting European fossil fuel demand to electricity load as a way to mitigate the crisis and the dependency it highlighted is in its prime moment.

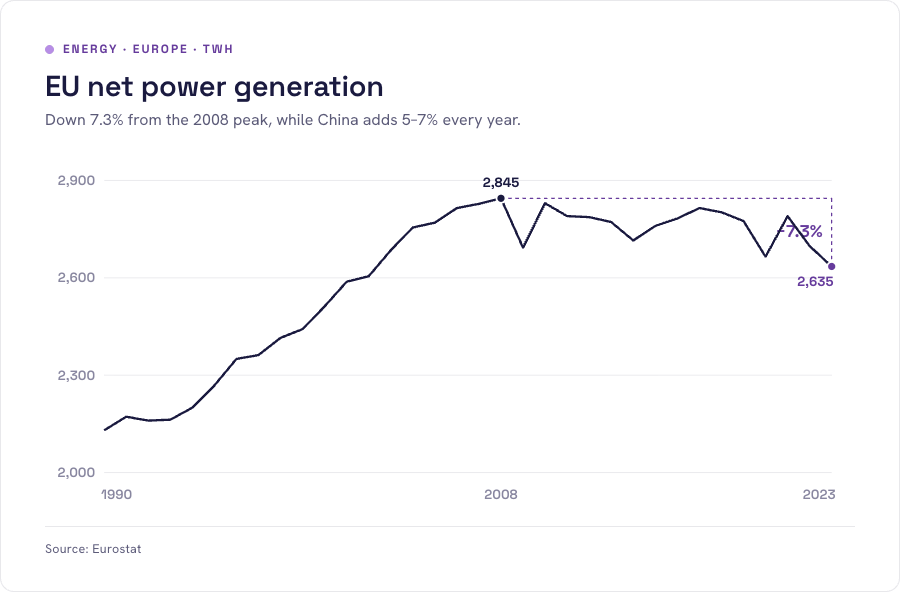

The re-escalating crisis will play strongly into EAP’s release, a leaked draft of which was covered extensively. The IEA Executive Director saying that Europe made a "major mistake" falling behind on electrification, with electricity's share in its final energy use around 23% for a decade gave it intellectual authority. He made a comparison to China, Japan, and Korea (though not the neighbouring Norway, whose share is among the highest in the OECD at roughly 49%). Add the incoming COP31 presidency's "35% by 2035" global electrification goal, announced in June, and the narrative’s momentum is undeniable.

As a small contextual aside, I came to learn and love electricity when working in a government transmission networks policy division, where I covered many of the topics the EAP includes (grids, storage, smart meters). That experience taught me about the risk that sits in the gap between directional policy documents and the 500-Thousand-Volt transmission line sagging in a heatwave, its capacity cut to avoid a blackout – closing that gap was my job.

Today, I continue to observe that the complexity in electricity – not just technologically, but perhaps even more so in its many market designs and regulatory regimes – often deters deep public debate and creates blind spot risk. I see some of the blind spots in the EAP, and that is why I wanted to do this brief.

The big picture and different views

"With decisive action at all levels, Europe can become the first electro-continent," the Commission says in the document, promising investments, savings and benefits well beyond the energy system. The draft casts the shift as a socio-economic, competitiveness and security imperative rather than a purely climate one, and expects demand-pull to translate into European factories and qualified jobs, singling out residential and industrial heat pumps.

The target number was not included in the leaked document, and reporting suggests a binding number will follow later this year in the post-2030 energy package, but there is an existing stated commitment to 32% by 2030 in the Clean Industrial Deal, so I will use that. If a 40% increase in just over three years strikes you as ambitious, many industry voices will disagree: the Electrification Alliance (Eurelectric, WindEurope, SolarPower Europe, the heat pump and e-mobility associations, and others) calls for binding electrification targets, and Eurelectric's own modelling points to 50-70% by 2050. Agora supports an EU target too, provided it comes with national and sectoral granularity, think tank Strategic Perspectives calls for a binding 50% by 2040, and over 100 companies with a combined $1.5 trillion in revenue have signed a call to make electrification a central pillar of industrial strategy.

Industry is not united, however: the Alliance of Energy Intensive Industries, the European Chemical Industry Council (Cefic) among them, opposes a percentage target altogether, arguing the plan should be judged on whether it delivers €50/MWh industrial electricity.

Either way, this is setting out to be an operationally consequential policy for everyone tied to Europe's energy system – suppliers, operators, financiers, consumers, and industry at large – so understanding its implications is important for your long-term positioning and bottom line.

With energy demand in Europe on an overall decline, particularly as industrial closures and relocations accelerate (see below), the increase in electricity's share comes not from connecting new customers but from converting existing demand from fossil fuels to electric technologies, and building the generation, transmission and distribution assets to meet it – all without any underlying "new demand". If successful, this also means volume loss for gas utilities already in a tough spot with reducing run times.

On the electrical side, given the size of today's European electricity system of about 1,162 GW according to Eurelectric, meeting the target would require more than 460 GW of firm generation and transmission assets (directional illustration; the build size is greater than demand to provide a reliability reserve and cover intermittency). For scale on the delivery side: Ember reports at least 120 GW of proposed renewable projects unable to connect because of grid constraints, and almost 700 GW sitting in connection queues across the eight countries that report queue data.

What are the blind spot risks?

The crisis context is the first blind spot: battered by two massive geopolitical energy shocks, Europe needs to act, and a reactive environment crowds out technical debate at the level an ambition this big needs.

Switching from risky imported fossil fuels to domestically produced, cleaner, cheaper renewables-based electricity seems like a no-brainer – more efficient, so you need less; cheap to run, so prices drop; industry happy, clean-tech manufacturing and jobs boom, energy secure, costs pay for themselves in savings.

Makes sense, but the premises need a closer look: that demand creates industry, that mandates are neutral, that moving taxes lowers costs, and that avoided imports pay for the build, and that the outcome is a more efficient, more prosperous economy. Can’t tackle all in a post, but will touch on the main ones.

Re-industrialisation and domestic clean-tech industry

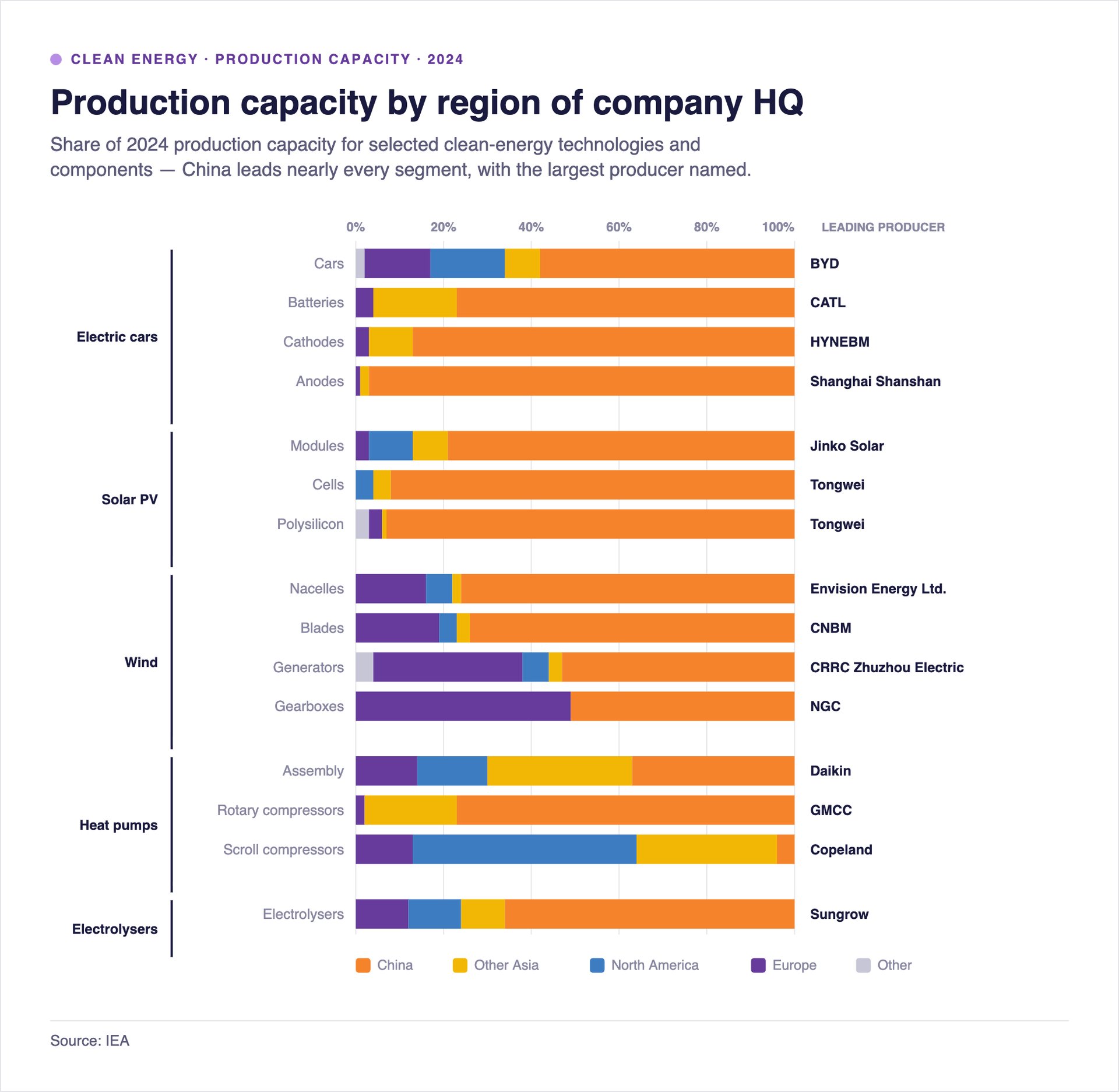

Local demand does not guarantee local industry – a lesson learnt in the Energiewende era. Demand creation grows deployment; it does nothing for supply chain competitiveness. Protective policies can try to force local content, but even setting trade rules aside, that significantly raises costs. Low-cost renewable technologies exist because China supplies them at a fraction of what it would take to produce them in Europe.

Meanwhile, Europe has been bleeding its traditional industries, and clean-tech remains a small share of total manufacturing – there is no clean category, but one proxy is roughly €40-50 billion in value added, which is about 2% of the EU's €2,500 billion manufacturing base. The prominent strengths, wind and power system components, are respectively under Chinese price pressure and dependent on upstream heavy industrial outputs. To be clear, they are important, but the potential trade-off with energy-intensive segments is a risk that should be taken more seriously. Per the IEA, none of the largest companies or production facilities across key clean energy supply chain segments in 2024 is in Europe.

According to the European Commission's 2025 report on the competitiveness of clean energy technologies:

Wind: still highly competitive, but under growing Chinese price pressure. In 2024 the EU held close to 13% of global manufacturing capacity in blades and nacelles and about 22% in towers; EU companies had close to 90% of the European market but 23% of the global one in 2023, down around 7% from 2022.

Batteries: about 7% of global output, dependent on China for cathodes and anodes – both critical.

Heat pumps: EU manufacturers lead in high-end domestic and industrial solutions, and assembly capacity is on track for 2030 needs – but key components, like compressors, are imported.

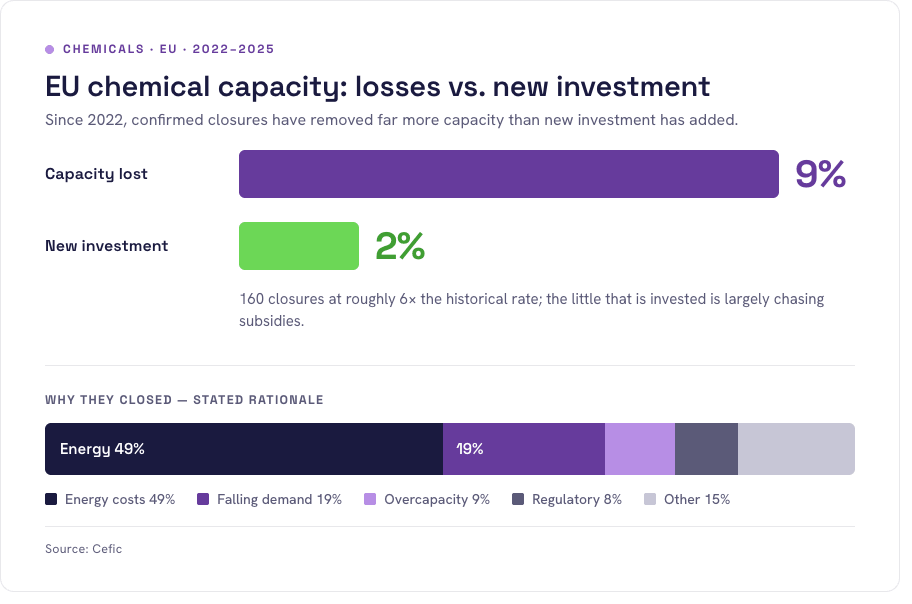

So the base the plan wants to build on is thin, and the existing base continues rapidly eroding. Cefic's closure radar counts 160 closures in 2022-2025 – totalling about 9% of European capacity by volume, with the annual pace increasing sixfold – against roughly 2% of capacity in new investment, much of it admittedly in the clean tech space. Energy costs were cited as the primary reason in half the announcements. The OECD reads the same way: chemicals the most affected sector, output down 10.3% between mid-2021 and mid-2024 to levels last seen in 2009, energy-intensive production down 12.4% and imports down 9.2% against 2021, and a trade balance in energy-intensive industries sliding toward deficit since 2012.

Neutral technology mandates

Despite an honourable mention of technological neutrality, there are plenty of technology-specific targets and mandates. Most are restated from previous documents, but there are some newbies:

Battery storage capacity from 55 GW to 200 GW by 2030 (restated)

Vehicle-to-grid requirement by 2027 (surprise, and can be a biggie)

Double heat pump installations by 2030

50% of final consumers on smart meters by 2031 to unlock demand response

100 GW of renewables deployed per year (restated)

Lowering prices through the "tax portion" of the bill

This is an area of market intervention, with things like "futureproofing electricity bills" and mandating a minimum electricity-to-gas price ratio. How the "tax portion" gets defined will matter, because the "non-energy" parts of the bill vary widely between member states and cover very different things.

The logic goes: electricity is too expensive, often at 3x+ the price of gas, so lower its relative cost, et voilà, a better business case. But the preceding question is why electricity costs so much in the first place. The non-energy component is what, in many cases, funds the existing system – operation, grid upgrades, reliability, and the incentives behind today's decarbonised power. If it moves off the bill, where does it go and who funds it? Shuffling the cost never addresses its cause. And the biggest risk of all is any price freeze or cap: it borrows from the future, compounding the existing problem further.

Lowering prices through the avoided fossil fuel import bill

The driving idea is that accelerated electrification could replace around two-thirds of Europe's gas demand and halve oil consumption by 2040, cutting the fossil fuel import bill by some €200 billion over the period – the leaked draft reportedly notes the EU spent an extra €50 billion on fossil imports during the 111-day Gulf crisis alone. The cost side is less specific, however. The plan rests on the proposition that the thing pays for itself, with benefits significantly outweighing costs. Whether an actual cost-benefit assessment was done at EU level, I don't know; if not, I would strongly push for one at national level. These calculations are better run on paper than learnt when the bill arrives.

The trouble with pay-for-itself logic is that someone still pays, and none of the stated measures is cheap. Smart metering and intelligent grids are excellent tools, for example, but rolling out a metering system that works securely, reliably, and actually delivers the energy goal is a bigger and more expensive task than it often seems.

The wrap

The final policy document lands on Friday, and the main thing to watch for is how much of it will turn into binding instruments vs aspiration. In addition to assessing it against the above questions, there is merit for impacted players to assess their own exposure and take advantage of the window before the binding version arrives.

This is a large topic, and one brief post cannot cover it fully. It is a topic Statem follows closely, so if you are looking to go deeper or want to understand better how to engage, I would love to hear from you.

Sources: IGU World LNG Report 2026 · Enerdata Yearbook · UNFCCC/COP31 Presidency (June 2026) · EUobserver (July 2026) · Clean Industrial Deal, COM(2025) 85 · Electrification Alliance (Nov 2025) · Eurelectric, Decarbonisation Speedways · Agora Energiewende (2026) · Strategic Perspectives (June 2026) · Alliance of Energy Intensive Industries (Feb 2026) · Ember, Crossed Wires (April 2026) · EC clean energy competitiveness report, COM(2025) 667 · IEA, Energy Technology Perspectives · Cefic/Roland Berger Closures Radar (Jan 2026) · OECD · Eurelectric electricity data · own estimates where indicated

The security argument behind the plan is implicated in this too. According to the IEA, China controls 60-85% of the five key clean energy technology supply chains – a far higher concentration than in oil and gas or most other strategic products. Substituting imported molecules with domestically generated electrons still means substituting one import dependency for another, at the equipment layer.

Want to receive these directly?

Building Smarter Energy Communications

© 2026. All rights reserved.

Send us a message, or

Book a free discovery call, or send us an email.

contact@statem.net